How Accurate Are Mortgage Calculators? What They Often Miss (2026)

Online mortgage calculators can be a useful starting point when you’re thinking about buying a home. Enter a home price, down payment, interest rate, and loan term, and within seconds you’ll see an estimated monthly payment.

The problem is that the number on your screen may not be the number you actually pay.

Some mortgage calculators estimate only principal and interest. Others attempt to include property taxes, homeowners insurance, and mortgage insurance but rely on generic assumptions that may have little to do with the home you’re considering or your actual financial situation.

For Michigan homebuyers, those differences can add hundreds of dollars to the true monthly housing payment.

That doesn’t mean mortgage calculators are useless. They’re actually a great tool for comparing different home prices, down payments, interest rates, and loan terms. You just need to understand what the calculator is—and isn’t—telling you.

In this guide, we’ll explain how mortgage calculators work, what they commonly leave out, why two borrowers purchasing the same-priced home can have very different payments, and how to estimate a more realistic monthly payment before making an offer.

Are Online Mortgage Calculators Accurate?

The short answer is: they can be accurate at calculating the information you give them, but the result is only as accurate as the assumptions being used.

Most basic mortgage calculators use three primary pieces of information:

- Loan amount

- Interest rate

- Loan term

With those numbers, a calculator can accurately estimate the principal and interest portion of a traditional fixed-rate mortgage payment.

But principal and interest are only part of the cost of owning a home.

Your actual monthly housing payment may also include:

- Property taxes

- Homeowners insurance

- Private mortgage insurance (PMI)

- FHA mortgage insurance

- HOA dues

- Flood insurance, when applicable

- Other property-specific expenses

The calculator may not know any of those numbers.

That’s where the difference between a mortgage calculation and an actual mortgage payment estimate becomes important.

What Does a Mortgage Payment Actually Include?

You’ll sometimes hear mortgage professionals use the term PITI, which stands for:

Principal + Interest + Taxes + Insurance

These are the primary components that typically make up a homeowner’s monthly mortgage-related payment.

Principal

Principal is the portion of your payment that reduces the amount you borrowed.

If you purchase a $400,000 home and make a $40,000 down payment, your starting loan amount would generally be $360,000 before considering any financed costs or program-specific items.

Interest

Interest is what you pay the lender for borrowing the money.

The interest rate used by an online calculator can create one of the biggest inaccuracies in the estimate because mortgage rates aren’t necessarily the same for every borrower.

Your actual rate can be affected by factors such as your:

- Credit profile

- Down payment

- Loan program

- Property type

- Occupancy

- Loan amount

- Mortgage term

- Market conditions when you lock your rate

The attractive rate you see advertised online may be available only under a particular set of assumptions. That’s one reason comparing an advertised rate with an actual Loan Estimate is so important when evaluating mortgage options.

Property Taxes

Property taxes are one of the most commonly misunderstood parts of online mortgage calculations, particularly for Michigan homebuyers.

A calculator may estimate taxes as a percentage of the home’s purchase price or use tax information associated with the property.

Neither necessarily tells you what your future property tax bill will be.

In Michigan, a home’s taxable value can change after a transfer of ownership. As a result, using the seller’s existing property tax bill to estimate what you’ll pay after purchasing the home can sometimes significantly underestimate your future housing expense.

This is an area where getting a property-specific estimate before purchasing can make a major difference.

Why the Same $400,000 Home Can Have Different Payments

This is where online calculators can become misleading.

Imagine two buyers are considering the exact same $400,000 home.

One buyer has a larger down payment, qualifies for a different interest rate, and doesn’t require mortgage insurance.

The other buyer makes a smaller down payment, has mortgage insurance, and qualifies for a slightly different interest rate.

They’re buying the same house for the same price, yet their monthly payments can be substantially different.

Now add differences in property taxes and homeowners insurance, and the gap becomes even larger.

That’s why asking “What’s the payment on a $400,000 house?” doesn’t really have one correct answer.

The better question is:

“What’s the payment on a $400,000 house based on my financing, this property’s taxes and insurance, and the loan program I’m actually using?”

That’s the number that matters when determining how comfortably a home fits into your budget.

Mortgage Calculator vs. Mortgage Pre-Approval

A mortgage calculator and a mortgage pre-approval serve two very different purposes.

A calculator lets you experiment with hypothetical numbers.

A mortgage pre-approval evaluates your actual financial situation.

Depending on the type and depth of the pre-approval, a mortgage professional may review factors such as:

- Income

- Employment

- Assets

- Credit

- Monthly debts

- Down payment

- Loan program

- Estimated property taxes and insurance

This allows the conversation to move beyond “What might the payment be?” and toward “What does this purchase realistically look like for me?”

That’s especially important before you begin seriously shopping for homes.

A calculator can help you explore.

A good pre-approval can help you plan.

What Mortgage Calculators Commonly Get Wrong

The biggest problem with online mortgage calculators isn’t usually the math.

It’s the assumptions.

A calculator can calculate principal and interest with remarkable precision, but if the interest rate, property taxes, homeowners insurance, mortgage insurance, or HOA dues entered into the calculation aren’t accurate, the final payment won’t be accurate either.

Here are some of the areas where online mortgage calculators most commonly miss the mark.

1. The Interest Rate May Not Be Your Interest Rate

Many online calculators automatically populate an interest rate or allow you to enter a rate you’ve seen advertised.

But mortgage rates aren’t one-size-fits-all.

The rate available to you can depend on several factors, including:

- Credit score and credit history

- Down payment

- Loan-to-value ratio

- Loan program

- Property type

- Occupancy

- Loan term

- Loan amount

- Whether you’re paying discount points

- Current market conditions

Even a relatively small difference in interest rate can noticeably change the payment on a larger mortgage.

There’s another important consideration: an advertised mortgage rate may include discount points or other assumptions that aren’t obvious from the headline rate.

That’s why comparing mortgage options based solely on the lowest advertised interest rate can be misleading. Looking at the interest rate, APR, lender costs, points, and overall loan structure provides a much better picture.

2. Property Taxes Can Be Significantly Underestimated

For Michigan buyers, this deserves special attention.

Some mortgage calculators pull the property’s current tax information from public records. Others simply estimate property taxes using a percentage of the home’s value.

The problem is that the seller’s current property tax bill isn’t necessarily what you’ll pay after purchasing the home.

Michigan property taxes involve taxable value, assessed value, and the Principal Residence Exemption (PRE), among other factors. When ownership transfers, the taxable value can potentially be uncapped for the following tax year, subject to Michigan’s property-tax rules.

That means a home that currently shows relatively low property taxes could have a noticeably different tax obligation after the purchase.

This can be especially important when the current homeowner has owned the property for many years and the home’s market value has increased substantially during that time.

A calculator using the seller’s current taxes may therefore make the future payment look more affordable than it actually will be.

For a serious purchase, we prefer to estimate what the taxes may look like after the transfer, rather than simply assuming the seller’s current tax bill will continue.

3. Mortgage Insurance May Be Missing or Incorrect

If you’re putting less than 20% down, you’ve probably heard that you’ll automatically have to pay PMI.

That’s not quite that simple.

On a conventional mortgage, private mortgage insurance can depend on several factors, including:

- Credit profile

- Down payment

- Loan-to-value ratio

- Loan characteristics

- Mortgage insurance provider

Two borrowers with the same purchase price and down payment don’t necessarily have identical PMI costs.

And putting less than 20% down doesn’t mean buying a home is automatically a bad idea. There are many situations where purchasing with a smaller down payment can make financial sense, particularly when preserving cash is important to the buyer.

FHA loans work differently and generally involve their own mortgage insurance structure, including an upfront mortgage insurance premium and an annual mortgage insurance premium paid monthly.

VA loans have another structure, and eligible borrowers generally don’t pay monthly mortgage insurance.

USDA loans also have their own guarantee-fee structure.

A generic calculator may not properly account for these differences, particularly if it doesn’t know which loan program you’re considering.

4. Homeowners Insurance Is Often Just a Guess

Homeowners insurance is another expense calculators frequently estimate using a generic number.

Actual premiums can vary considerably depending on the property and borrower.

Factors may include:

- Home value

- Location

- Age of the home

- Roof age and condition

- Construction characteristics

- Coverage limits

- Deductible

- Claims history

- Insurance carrier

If the calculator assumes $125 per month but your actual homeowners insurance is $225 per month, your estimated housing payment is already off by $100.

That’s why we prefer using a realistic insurance estimate when determining affordability rather than relying on a generic national assumption.

5. HOA Dues May Be Completely Missing

Buying a condominium or a home in a homeowners association?

Don’t forget the HOA payment.

Depending on the community, HOA dues might be $50 per month, $300 per month, or considerably more.

Even when HOA dues aren’t technically part of your mortgage payment, lenders generally consider required association dues when evaluating your monthly obligations and debt-to-income ratio.

A calculator that ignores a $300 monthly HOA fee can make a property look significantly more affordable than it actually is.

This is also why buyers should consider the entire cost of owning a particular property—not simply principal and interest.

6. The Calculator Doesn’t Know Your Loan Program

One of the biggest weaknesses of a generic mortgage calculator is that it doesn’t necessarily know which financing strategy makes the most sense for you.

A buyer might qualify for:

- Conventional financing

- FHA financing

- VA financing

- USDA financing

- Down payment assistance

- Other specialized mortgage programs

Those programs can have different:

- Down payment requirements

- Mortgage insurance structures

- Funding or guarantee fees

- Qualification requirements

- Interest-rate characteristics

A calculator may tell you what one hypothetical mortgage looks like without showing you that another financing option could produce a very different result.

That’s one of the advantages of working with an independent mortgage broker. Rather than simply calculating one loan scenario, we can compare available financing strategies and help determine which structure makes sense for your circumstances.

7. A Lower Payment Doesn’t Always Mean a Better Mortgage

This is another area where calculators can oversimplify the decision.

Suppose one scenario produces a payment that’s $75 lower each month.

Sounds better, right?

Maybe.

But what if obtaining that payment requires several thousand dollars in discount points?

What if another option has a slightly higher payment but substantially lower upfront costs?

What if putting additional money down lowers your payment but leaves you with very little savings after closing?

Mortgage decisions involve trade-offs.

The goal isn’t necessarily to create the lowest possible monthly payment at any cost.

The goal is to find a mortgage structure that makes sense for your budget, cash position, expected time in the home, and long-term financial goals.

That’s something a basic online calculator simply can’t evaluate for you.

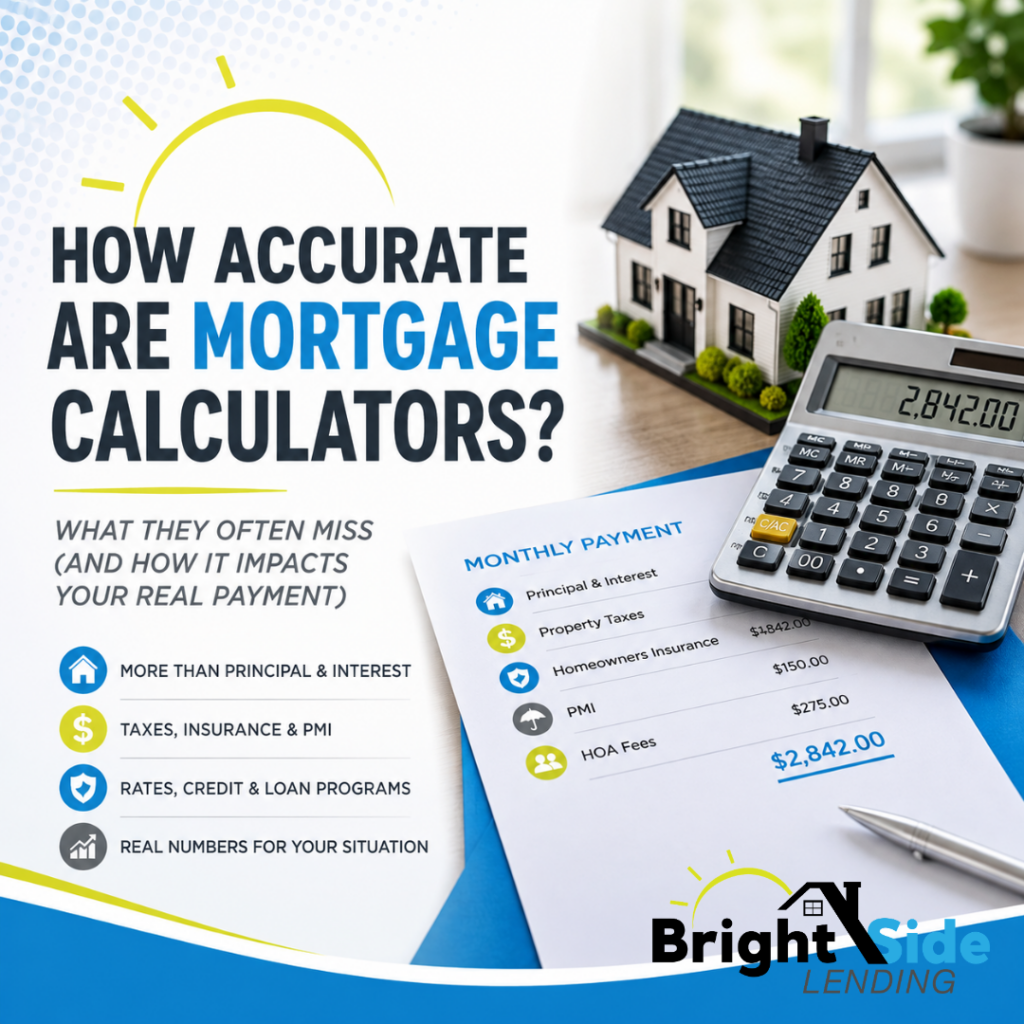

A Realistic Example: Online Calculator Payment vs. Actual Mortgage Payment

Let’s look at an example of why the payment you see online can be very different from the payment you ultimately receive when financing a home.

Suppose you’re considering purchasing a home in Michigan for $400,000.

You enter the following information into an online mortgage calculator:

- Purchase price: $400,000

- Down payment: 10%

- Loan amount: $360,000

- Loan term: 30 years

- Interest rate: 6.50%

The calculator estimates principal and interest at approximately $2,275 per month.

You might look at that number and think:

“Great. A $400,000 home costs me about $2,275 per month.”

But that’s not your complete housing payment.

Now let’s add some of the expenses that a basic calculator may have excluded or estimated incorrectly.

Example of a More Complete Monthly Payment

| Monthly Expense | Example Amount |

|---|---|

| Principal & Interest | $2,275 |

| Property Taxes | $650 |

| Homeowners Insurance | $175 |

| Mortgage Insurance | $125 |

| Estimated Total Housing Payment | $3,225 |

That’s a difference of approximately $950 per month between the principal-and-interest calculation and the more complete estimated housing payment.

Over a year, that’s an $11,400 difference in cash flow.

These numbers are only examples—the actual taxes, insurance, mortgage insurance, interest rate, and other costs would depend on the borrower and property—but they illustrate why it’s important to understand exactly what an online calculator is showing you.

And if the property has a $250 monthly HOA fee?

Your total monthly housing expense could be closer to $3,475.

The calculator wasn’t necessarily wrong when it showed $2,275.

It simply wasn’t answering the question you thought you were asking.

What Should You Enter Into a Mortgage Calculator?

Mortgage calculators become much more useful when you give them realistic information.

If you’re using one to determine whether a particular home may fit your budget, try to gather the following information first:

Purchase Price

This one is straightforward.

Use the actual asking price or the price you’re considering offering for the property.

If you’re still early in the process, try several purchase prices to see how different price ranges affect your estimated payment.

Down Payment

Don’t automatically enter 20% just because you’ve heard that’s what you’re “supposed” to put down.

Many mortgage programs allow significantly smaller down payments.

The appropriate amount depends on your loan program, available savings, financial goals, and how much money you want to keep available after closing.

For some buyers, putting 20% down makes sense.

For others, putting less down and maintaining a larger emergency fund may be the better financial decision.

Realistic Interest Rate

Avoid automatically using the lowest mortgage rate you find advertised online.

If you’re already working with a mortgage professional, use a rate that’s reasonably representative of your situation.

If you’re just beginning your research, understand that the rate you’re entering is an assumption—not a quote or guarantee.

You can also use the calculator to see how different rates affect affordability.

For example, compare the payment at:

- 6.00%

- 6.50%

- 7.00%

This can help you understand how sensitive your budget is to changes in mortgage rates.

Don’t Forget Property Taxes

This is particularly important when buying a home in Michigan.

Rather than simply copying the seller’s current property tax bill into the calculator, try to obtain an estimate of what the property taxes may look like after the transfer of ownership.

The difference can sometimes be substantial.

If you’re looking at homes in different communities, property taxes can also change considerably from one municipality or school district to another.

Two homes with identical $400,000 purchase prices could therefore have noticeably different monthly housing payments.

That’s one reason evaluating affordability based only on purchase price can be misleading.

Use a Realistic Homeowners Insurance Estimate

If possible, obtain an insurance quote for the property before you’re too far into the transaction.

You don’t necessarily need an exact insurance premium when you’re casually browsing homes, but using a realistic estimate will produce a much better calculation than accepting whatever generic number a website automatically inserts.

Once you’re under contract, getting an actual quote allows the mortgage payment estimate to become considerably more precise.

Include Mortgage Insurance When Applicable

If you’re considering a smaller down payment, make sure the calculator accounts for the appropriate type of mortgage insurance or program-specific fee.

This becomes particularly important when comparing FHA and conventional financing.

A conventional mortgage and an FHA mortgage on the same house can have different:

- Interest rates

- Down payments

- Mortgage insurance costs

- Upfront costs

- Monthly payments

Rather than assuming one program is automatically cheaper, it’s better to compare the complete financing scenarios side by side.

Include HOA Dues

If the property has mandatory HOA or condominium association dues, include them in your affordability calculation.

Even though the HOA payment may be made separately from your mortgage payment, it’s still money leaving your household every month.

More importantly, lenders generally consider required HOA dues when determining whether you qualify for the mortgage.

Ignoring them can make both your estimated payment and your estimated purchasing power look better than they really are.

Mortgage Payment vs. How Much Home You Can Afford

There’s another important distinction that online calculators don’t always make clear.

Just because a calculator shows that you can make the payment doesn’t necessarily mean that’s the price range you should purchase in.

Mortgage qualification and personal affordability aren’t exactly the same thing.

A lender evaluates factors such as your income, debts, assets, credit profile, and applicable loan guidelines to determine what you may qualify to borrow.

But the lender doesn’t know everything about your lifestyle.

Maybe you:

- Travel frequently

- Have significant childcare expenses

- Want to continue contributing aggressively to retirement

- Have private-school tuition

- Own expensive hobbies or recreational vehicles

- Want to maintain a large emergency fund

- Simply don’t want to spend the maximum amount possible on housing

Those considerations matter.

Being approved for a certain mortgage amount doesn’t mean you need to spend that much.

At BrightSide Lending, we would rather help you understand several payment and purchase-price scenarios than simply tell you the maximum mortgage amount you could potentially qualify for.

The best mortgage isn’t necessarily the largest mortgage available.

It’s the one that helps you purchase the right home while keeping the rest of your financial life comfortable.

Are Mortgage Calculators Good for First-Time Homebuyers?

Yes—as long as you understand their limitations.

For a first-time homebuyer, a mortgage calculator can be one of the easiest ways to begin understanding the relationship between:

- Home price

- Down payment

- Interest rate

- Loan amount

- Loan term

- Monthly payment

It can also help answer useful early-stage questions.

What happens to my payment if I buy a $300,000 home instead of a $350,000 home?

How much would another $20,000 down change my payment?

What happens if mortgage rates move half a percentage point?

Would a 15-year mortgage fit my budget, or is a 30-year mortgage more comfortable?

Those are exactly the types of questions mortgage calculators are good at answering.

The mistake is treating the result as a mortgage quote or pre-approval.

If you’re preparing financially for your first home purchase, use a calculator for planning and education. Once you’re seriously considering homes, it’s time to replace the generic assumptions with numbers based on your actual financial situation.

Can a Mortgage Calculator Tell Me How Much I Qualify For?

Not reliably.

Some online calculators include a “How much house can I afford?” feature. These tools typically ask for information such as:

- Annual income

- Monthly debts

- Down payment

- Interest rate

- Estimated property taxes

- Homeowners insurance

The calculator then uses a predetermined debt-to-income ratio to estimate a maximum home price.

That can provide a rough starting point, but mortgage qualification is more complicated.

Different loan programs can have different qualification guidelines. The way income and debts are calculated can also vary depending on the situation.

For example, qualification may be affected by:

- Student loans

- Auto loans

- Credit card balances

- Alimony or child support obligations

- Self-employment income

- Bonus, commission, or overtime income

- Rental property income

- Existing mortgages

- Property taxes

- HOA dues

- Credit history

- Available assets

A calculator doesn’t underwrite your mortgage application.

That’s why someone shouldn’t eliminate a home from consideration—or assume they qualify for one—based solely on an online affordability calculator.

What About Self-Employed Homebuyers?

This is another situation where online affordability calculators can be particularly misleading.

A self-employed borrower might know exactly how much money their business generates each year, but that doesn’t necessarily mean a mortgage lender will use the same income figure.

Traditional mortgage qualification for self-employed borrowers can involve reviewing tax returns and applying applicable underwriting guidelines to determine qualifying income.

There are also situations where a self-employed borrower may explore alternatives such as bank statement loans, which can evaluate income differently than a traditional conventional mortgage.

An online calculator generally doesn’t understand any of this.

It simply asks:

“What’s your annual income?”

For a salaried employee with straightforward income, that may be relatively easy to answer.

For a business owner, independent contractor, or borrower with multiple sources of income, it may be much more complicated.

Mortgage Calculators Can’t Evaluate Your Credit

Your credit profile can influence both mortgage qualification and pricing.

A calculator doesn’t pull your credit report when you casually enter numbers online, nor would you want every calculator you visit to do so.

That means it usually has no idea whether the rate being used is appropriate for your credit profile.

If you’re several months away from purchasing, this can actually be useful information.

Reviewing your credit early gives you time to identify potential issues and, when appropriate, take steps to improve your credit before applying for a mortgage.

Even relatively small improvements can sometimes expand your financing options.

Be Careful With “Today’s Mortgage Rate” Calculators

You’ve probably seen websites advertising something similar to:

“See Today’s Mortgage Rate!”

You enter a purchase price and maybe your ZIP code, and suddenly an attractive interest rate and payment appear.

Pay attention to the assumptions.

That advertised rate may assume:

- Excellent credit

- A specific down payment

- A particular loan amount

- Owner-occupied financing

- A particular property type

- Payment of discount points

- Specific loan terms

That doesn’t necessarily mean there’s anything improper about the advertised rate.

It simply means you need to understand the assumptions behind it.

A mortgage rate without the accompanying costs and loan structure doesn’t tell you enough to determine whether you’re getting a good deal.

The Difference Between Interest Rate and APR

This is another area where online mortgage shoppers can get confused.

The interest rate is used to calculate the interest portion of your mortgage payment.

The annual percentage rate (APR) is designed to reflect certain costs associated with obtaining the loan in addition to the interest rate.

APR can be useful when comparing mortgage offers, but it isn’t the same thing as your interest rate and it isn’t your monthly payment.

For example, two lenders could advertise the same interest rate while charging very different amounts in discount points or lender fees.

That’s why borrowers should compare the complete financing offer rather than focusing exclusively on whichever website advertises the lowest rate.

Once you’re formally shopping for a mortgage, the Loan Estimate becomes an especially useful tool because it provides a standardized way to compare important loan terms and costs.

Should You Enter Your Information Into an Online Mortgage Calculator?

Sometimes—but know who you’re giving it to first.

A basic calculator that simply lets you enter numbers and see a payment doesn’t necessarily need your:

- Name

- Email address

- Phone number

If a website requires that information before showing your results, understand what may happen after you click submit.

Some mortgage and real estate websites use calculators as lead-generation tools. Depending on the company’s privacy practices and the consent you provide, your information may be used to connect you with mortgage providers or other businesses.

That can result in calls, emails, or text messages from companies you weren’t expecting to hear from.

Before submitting personal information, read what you’re agreeing to.

At BrightSide Lending, when you contact us directly about your mortgage, we’re interested in helping you evaluate your financing—not turning your information into a product to sell to unrelated companies.

When Should You Stop Using a Calculator and Talk to a Mortgage Professional?

There’s no need to call a mortgage professional every time you’re curious about what a $500,000 mortgage payment might look like.

That’s exactly what calculators are for.

But there comes a point where generic estimates stop being useful enough.

Consider getting personalized numbers when:

- You’re planning to buy within the next several months

- You’re actively looking at homes

- You’re unsure how much you should put down

- You’re comparing FHA and conventional financing

- You’re eligible for VA or USDA financing

- You’re self-employed

- You’re concerned about your credit

- You own another property

- You’re trying to buy before selling your current home

- You need to know your realistic maximum purchase price

- You’re ready to make an offer

At that stage, the difference between an estimate and an actual financing strategy becomes important.

Frequently Asked Questions About Mortgage Calculators

Do mortgage calculators include property taxes?

Some do and some don’t. Even calculators that include property taxes may use an estimated amount or the property’s existing tax information. For Michigan homebuyers, it’s important to consider how taxes may change following a transfer of ownership rather than automatically relying on the seller’s current tax bill.

Do mortgage calculators include PMI?

Some calculators estimate private mortgage insurance when the down payment is below 20%, but the actual cost of PMI can vary. FHA, VA, USDA, and conventional loans also handle mortgage insurance or program fees differently.

Why is my lender’s mortgage payment higher than the online calculator?

The lender’s estimate may include expenses the online calculator omitted or underestimated, such as property taxes, homeowners insurance, mortgage insurance, or HOA dues. The interest rate used by the calculator may also differ from the rate available for your actual financing scenario.

Are Zillow and other online mortgage calculators accurate?

They can be useful for estimating principal and interest and providing a general starting point. However, any calculator’s accuracy depends on the assumptions being used for the interest rate, taxes, insurance, mortgage insurance, HOA dues, and loan program. For an actual home purchase, property-specific and borrower-specific numbers provide a much more meaningful estimate.

Can a mortgage calculator tell me how much house I can afford?

It can provide an estimate, but it can’t determine exactly how much mortgage financing you qualify for. Mortgage qualification involves your income, debts, assets, credit, loan program, and applicable underwriting guidelines.

Does using a mortgage calculator affect my credit?

Simply using a calculator and entering hypothetical numbers does not require a credit inquiry. If you proceed to a mortgage application or authorize a lender to obtain your credit report, that’s different.

The Bottom Line: Use Mortgage Calculators as a Starting Point, Not the Final Answer

Mortgage calculators aren’t bad tools.

They’re actually very useful tools when they’re used for the right purpose.

Use them to experiment.

Use them to compare home prices.

Use them to see how different down payments or interest rates could affect principal and interest.

Use them to begin building a home-buying budget.

Just don’t mistake an online estimate for a personalized mortgage analysis.

The true cost of buying a home depends on much more than the purchase price and interest rate. Property taxes, homeowners insurance, mortgage insurance, HOA dues, loan program, credit profile, down payment, and other factors can all affect the final numbers.

For Michigan homebuyers, understanding those details before making an offer can help prevent one of the most frustrating experiences in the home-buying process: discovering that the payment you planned around isn’t the payment you’re actually going to have.

At BrightSide Lending, our goal isn’t simply to tell you the maximum amount you might qualify to borrow. We can compare financing options, estimate the complete monthly payment, and help you understand how different purchase prices, down payments, and loan programs affect your overall financial picture.

If you’re still researching, keep using the calculators.

When you’re ready for the numbers to become real, that’s when it’s time to build an actual mortgage strategy. In the meantime, you can also explore our Mortgage Resource Center.